The Death of Per-Seat Pricing —

Why AI Agents Are Breaking the SaaS Revenue Model

Every SaaS vendor’s growth model was built on one assumption: more employees means more seats means more revenue. That assumption is now wrong — and the market has started pricing in the consequences.

-

15% ReversingShare of SaaS companies using pure per-seat pricing — down from 21% in twelve months — Growth Unhinged, 2025 State of B2B Monetisation

-

$285B ReversingWiped from SaaS valuations in 48 hours in February 2026 — the largest AI-triggered repricing event in software history — SaaSpocalypse analysis, Taskade

- Of SaaS companies on hybrid pricing models — up from 27% in twelve months — Growth Unhinged, 2025

-

320% ConfirmedGrowth in total AI-driven spend — even as token prices fell 80% year over year — BetterCloud 2026 SaaS Industry Report

- Per resolved ticket — Intercom Fin — grew from $1M to $100M ARR in 24 months on pure outcome-based pricing — GTMnow via Bhavishya Pandit, 2026

For twenty-five years, SaaS revenue grew on the back of a single number: headcount. Every new hire was a new seat. Every new seat was new ARR. The model was so reliable that investors learned to value SaaS companies on multiples of it — because they could predict the future with unusual confidence. Headcount went up. Software spend followed.

That relationship is breaking. Not gradually. Not theoretically. In February 2026, $285 billion in SaaS valuation was wiped in 48 hours — not because companies reported bad revenue, but because investors collectively concluded the model itself was mispriced. AI agents were already doing work that used to require human logins. The seat count was already wrong. The question was only when the market would notice.

Who this is for: SaaS founders assessing their pricing exposure · Operators evaluating vendor contracts · Investors modelling NRR risk in software portfolios

The Seat Paradox: When Customer Success Destroys Vendor Revenue

THE STRUCTURAL BREAK THAT CHANGES EVERYTHINGHere is the problem that per-seat pricing cannot survive. A company deploys AI agents to handle customer support. The agents work. Ticket resolution time drops. Support quality improves. The company is delighted. And then renewal comes — and they cut 60 support seats. Their vendor loses 60 × $X per month. The customer’s success has directly cannibalised their vendor’s revenue. This is not an edge case. It is the new default trajectory of any well-deployed AI system.

The logic of per-seat pricing was always a proxy. Vendors could not easily measure whether their software was producing outcomes — closed deals, resolved issues, processed invoices — so they measured the thing that correlated with outcomes: how many humans were logging in. That proxy held for twenty-five years. It fails the moment agents begin replacing those logins. Arnon Shimoni of Paid.ai frames it precisely: seat pricing didn’t just die — its margins migrated. The value once captured in human licences now lives in compute bills.

Agent deployment reduces the human headcount needed to complete a fixed volume of work. Headcount reduction eliminates seats. Seat elimination cuts ARR. The better the AI deployment performs, the steeper the seat reduction. This is the Seat Paradox — the model actively punishes vendors whose products work best. MindStudio’s analysis documents 30–90% seat reductions in first-wave AI deployments across customer support, SDR, and back-office categories.

Klarna publicly eliminated 700 customer service roles via AI in 2024 — and every software vendor whose products those 700 people used absorbed the revenue loss silently. Monday.com replaced 100 SDRs with AI agents in early 2026. Workday — a company that sells workforce management software — cut 8.5% of its own headcount because of AI. According to Zylo’s 2026 SaaS Management Index, the average enterprise already wastes $21M per year on unused licences — a 14.2% increase in a single year, driven partly by AI-induced headcount compression.

Ask yourself one question: if your product works perfectly, does your customer need fewer human employees to use it? If yes, your per-seat pricing is structurally misaligned with the value you deliver. The earlier you identify this, the more options you have. Waiting for NRR to fall before diagnosing the cause is expensive. Read our SaaS Metrics Explained guide to understand how NRR compression propagates through your valuation.

The SaaSpocalypse: When $285 Billion Validated the Thesis in 48 Hours

THE MARKET EVENT THAT MADE THE RISK REALOn February 3, 2026, investors began pricing in what analysts had been warning about for months. In a 48-hour window, approximately $285 billion was wiped from SaaS company valuations — the largest AI-triggered repricing event in software history. The financial press called it the SaaSpocalypse. But the name obscures the mechanism. This was not a panic. It was a reclassification. Wall Street had stopped treating AI disruption as a distant risk and started pricing it as an immediate structural reality.

The immediate catalyst was Anthropic’s launch of Claude Cowork — a product demonstrating AI agents performing sustained, multi-step knowledge work across CRM platforms, support systems, analytics dashboards, and project management tools without continuous human input. The demonstration was not aspirational. It was operational. And it answered the question investors had been asking: if AI agents become the primary users of software, how sustainable is per-seat pricing? The answer the market gave was: not very.

The selloff was not uniform. It targeted seat-dependent companies whose revenue models were most exposed to agent-driven headcount compression. Atlassian reported its first-ever decline in enterprise seat counts. By March 2026, public B2B software equities had compressed 25% year-to-date — the sharpest correction since the 2022 interest rate hikes — with AI-native companies trading at 10–40x revenue and traditional SaaS below 5x.

The contrarian case is worth noting. Bank of America analyst Vivek Arya called the selloff “overblown and logically inconsistent.” PYMNTS reported that No Jitter analyst Dave Michels observed AI agents still need licences for the tools they operate through — Salesforce, Slack, Microsoft 365. The nuance is real: not all SaaS is equally exposed. Tools that agents use as infrastructure are defensible. Tools that agents replace humans in using are not.

The February event revealed a vulnerability spectrum. Companies building in categories where agents replace human users — support, sales development, compliance review, document processing — are in the Disrupted quadrant regardless of current revenue. Companies selling infrastructure that agents depend on are Defensible. The question every SaaS founder must answer now: is my product a tool that agents use, or a seat that agents replace? See our B2B SaaS Trends 2026 analysis for the full landscape.

What triggered the $285B SaaSpocalypse selloff in February 2026?

The NRR Trap: How Seat Compression Collapses Valuation Multiples

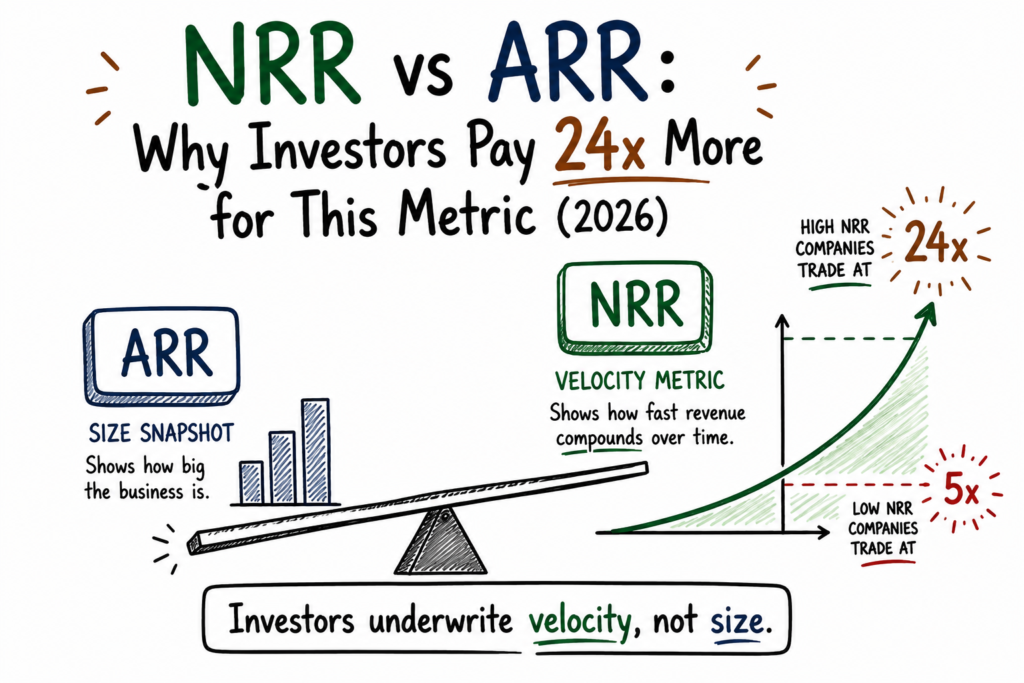

THE FINANCIAL MECHANISM BEHIND THE REPRICINGNet revenue retention is the metric that justifies premium SaaS valuations. When NRR stays above 110%, investors reward it with double-digit ARR multiples because the model is effectively compounding: existing customers automatically spend more over time as their headcount grows. Per-seat pricing has always relied on this expansion motion. As Jason Lemkin of SaaStr put it plainly: “If 10 AI agents can do the work of 100 reps, you need 10 Salesforce seats, not 100.” When that compression happens, NRR doesn’t just flatten — it reverses.

The token pricing paradox compounds the problem for vendors. BetterCloud’s 2026 SaaS Industry Report documents a counterintuitive dynamic: even as token prices fell 80% year over year, total AI-driven spending grew 320%. This means consumption volume is dramatically outpacing unit price declines — and vendors who bundle unlimited AI into a flat per-seat fee are subsidising their heaviest users. Simon-Kucher documented cases where heavy AI users generated compute costs several multiples above their subscription price — making specific products loss-making under flat-fee models.

Per-seat SaaS has a compounding NRR assumption baked into its valuation. That assumption requires headcount to grow over time. AI inverts this: customers who deploy agents most aggressively shrink their headcount fastest. The best customers — the ones doing the most with the product — become the ones generating the least revenue. This is not a temporary dip. It is a structural reversal of the expansion motion that justified premium multiples for twenty years.

According to Bain’s analysis of 30+ SaaS vendors introducing AI capabilities, 35% simply increased per-seat pricing and bundled AI features in. This is “structurally vulnerable” — agents operating at 10x human volume under the same licence cost will eventually make these products loss-making as compute costs rise. AI-native companies now trade at 10–40x revenue multiples. Traditional per-seat SaaS sits below 5x. That gap is not sentiment — it is the market pricing in different NRR trajectories.

Model this scenario now: your top 10 customers each cut seat counts by 40% over 18 months as they deploy AI agents. What happens to your NRR? If it drops below 100%, your current valuation multiple is unsupported. This is not a stress test — it is the median trajectory for any per-seat SaaS company in a category with high AI agent penetration. Understanding your NRR, ARR, and LTV metrics is the starting point for this analysis.

The Three Pricing Models Fighting to Replace Per-Seat

CONSUMPTION, OUTCOME, AND HYBRID — RISK PROFILES FOR BOTH SIDESThere is no single pricing model winning the transition. Three models are competing, each with different risk profiles for buyers and sellers. The right model depends on what your software actually produces, your ability to measure it, and your tolerance for revenue volatility. The comparison table below maps the key variables across all three — use it as a decision tool, not a leaderboard.

What runs through all three alternatives is a single principle: value tracks work done, not humans doing it. The era of selling logins is ending. The era of selling outcomes — or at minimum, consumption of capabilities — has begun. Paid.ai’s analysis identifies hybrid as a “pause button” — it stabilises revenue while the per-seat component slowly loses ground. That is not wrong. Hybrid is where most of the industry is landing in 2026.

| Model | Unit of Billing | Who’s Using It | Vendor Risk | Buyer Risk | NRR Outlook |

|---|---|---|---|---|---|

| Per-Seat | Human login | Salesforce, Atlassian, Slack | Seat compression as AI replaces humans | Overpaying for unused licences | Declining (structural) |

| Consumption / Usage-Based | API calls, tokens, tasks | Snowflake, AWS, Anthropic | Revenue unpredictability; margin at scale | Budget volatility; runaway costs | Scales with usage |

| Outcome-Based | Resolved ticket, closed deal, processed invoice | Intercom Fin, Salesforce Agentforce, Sierra AI | Measurement complexity; attribution disputes | Vendor controls outcome definition | Aligns with value delivered |

| Hybrid | Platform fee + variable usage | ServiceNow, HubSpot, Microsoft Copilot | Fixed base still exposed to seat compression | Complexity in forecasting variable component | Transitional — stabilising |

| Agent-Based | Per agent / per month (synthetic labour) | Sierra AI, emerging agent platforms | Compute cost per agent hard to forecast | Governance of autonomous spending | Emerging — high potential |

Consumption pricing scales revenue with usage volume — transparent but volatile. Outcome pricing charges for results — aligned but hard to measure. Hybrid pricing adds a variable component to an existing seat base — stabilising but not structural. Agent-based pricing treats autonomous agents as synthetic labour — coherent in theory, early in practice. Most SaaS companies are not choosing between these models; they are migrating through them, with hybrid as the current landing zone.

Intercom Fin charges $0.99 per resolved conversation and grew from $1M to $100M ARR in 24 months — validating outcome pricing at scale. Salesforce Agentforce charges $2 per AI-handled conversation. PYMNTS reported that Salesforce and HubSpot are both preparing to expand outcome-based pricing components across their product suites. Adobe announced outcome-based pricing for its AI products suite (Adobe CX Enterprise) in April 2026.

The transition is not optional — it is a question of timing and sequencing. Three steps before selecting a model: (1) Identify your actual unit of value — not who uses the product, but what the product produces. (2) Calculate your compute floor — know your LLM API cost per unit of value before pricing it. (3) Grandfather existing customers — never force abrupt transitions from predictable to variable billing. The Pricing Model Selector below maps your situation to the right model.

“If 10 AI agents can do the work of 100 reps, you need 10 Salesforce seats, not 100. The maths is brutally simple.”— Jason Lemkin, Founder, SaaStr — via The Payers, May 2026

How the Biggest Vendors Are Responding — and What It Reveals

THE STRATEGIC MOVES WORTH WATCHING IN 2026The vendors moving fastest are the ones with the most to lose from inaction. Salesforce is arguably the most seat-dependent major SaaS company in enterprise software. Their entire revenue model — CRM, Service Cloud, Sales Cloud — runs on the assumption that more human users equals more spend. By launching Agentforce with a per-conversation pricing model, they are acknowledging that the old motion is structurally at risk and trying to replace it with something that grows with AI deployment rather than shrinking because of it.

ServiceNow has moved toward consumption models tied to workflow executions rather than seats. Workday has explored outcome-linked components for certain modules. Microsoft’s Copilot pricing created a hybrid — a seat add-on on top of existing seats — which works in the short term but does not solve the problem when agents start replacing the humans paying for the base seats. According to Trending Topics’ May 2026 analysis, the “token tax” is forcing every vendor to price in compute costs they previously ignored.

| Vendor | Old Model | New / Announced Model | Strategic Signal |

|---|---|---|---|

| Salesforce (Agentforce) | Per seat (CRM, Service Cloud) | $2 per AI conversation | Outcome pricing at enterprise scale |

| Intercom (Fin) | Per seat (support platform) | $0.99 per resolved ticket | Fastest outcome-pricing ramp in SaaS history |

| Microsoft (Copilot) | Per seat (M365) | $30/user add-on (M365 required) | Hybrid holding pattern; seat base still exposed |

| ServiceNow | Per seat (ITSM workflows) | Consumption per workflow execution | Transitioning toward execution-based billing |

| Adobe (CX Enterprise) | Per seat (Creative Cloud, Marketing) | Outcome-based for AI products | Announced April 2026 — category signal |

| HubSpot | Per seat / tiered | Outcome-based components in preparation | Reported by The Information, April 2026 |

The vendors moving fastest are signalling the depth of their internal seat compression modelling. When the most seat-dependent company in enterprise software (Salesforce) launches a per-conversation pricing tier, it is not an innovation play — it is a hedge. They have run the numbers on what agent-driven headcount compression does to their ARR five years out and decided to move before the market forces them to. Every SaaS company still sitting on pure per-seat pricing is implicitly betting that seat compression won’t reach their category before their next repricing window.

Intercom Fin is the clearest evidence of outcome pricing at scale: $1M to $100M ARR in 24 months, handling over 1 million tickets per week, with a performance guarantee of up to $1M if the agent misses resolution targets (GTMnow, February 2026). Sierra AI reached $100M ARR faster than any AI company in history by pricing agents as synthetic labour. These are not pilots. They are production-grade commercial models with verified scale.

Watching the large vendors move is not enough. By the time Salesforce’s Agentforce pricing becomes the category default, you have missed the window to differentiate on model design. First-movers in outcome pricing within a given vertical have a structural advantage: they attract the customers most aggressively deploying agents — the fastest-growing, most innovative enterprises. Those are the customers every SaaS company wants.

Per-Seat Era vs. Agent Era: What Changed and What Didn’t

EIGHT SHIFTS THAT DEFINE THE TRANSITIONThe seat was never the point. It was a proxy for value — a proxy that held for twenty-five years because headcount and software usage happened to correlate. AI agents broke the correlation. The seat count is now an actively misleading metric: it understates the value that AI-enabled teams deliver and overstates the number of licences those teams need. The vendors who survive this transition will be the ones who found the real unit of value before the market forced them to.

Find Your Pricing Model: The SaaS Transition Selector

FIVE SCENARIOS — ONE RECOMMENDED MODEL FOR EACHUsage-Based / Consumption

Examples: Snowflake · AWS · Anthropic API · StripeAPI and infrastructure tools have clear, measurable consumption units — API calls, tokens, data processed, transactions. Revenue scales with usage volume, which scales with agent activity. This model is already the default for AI infrastructure and translates well to any tool where usage volume is the natural value metric.

Outcome / Resolution-Based

Examples: Intercom Fin ($0.99/ticket) · Salesforce Agentforce ($2/conversation)Customer support is the most advanced category for outcome pricing. Resolution is a clean, measurable outcome. Intercom Fin validated this at $100M ARR in 24 months. The outcome definition — “resolved conversation” — is accepted by both sides. Support AI that replaces human agents is the clearest case for abandoning per-seat immediately.

Hybrid: Platform Fee + Outcome Component

Examples: Salesforce (seat + Agentforce add-on) · HubSpot (preparing transition)CRM is the hardest category for pure outcome pricing. “A closed deal” involves too many variables — sales cycle length, territory, product mix — to attribute cleanly to a single tool. Hybrid works here: a platform fee covers data, infrastructure, and access. An outcome component (per qualified meeting, per pipeline opportunity opened) captures agent-generated value without requiring full attribution.

Outcome / Transaction-Based

Examples: HighRadius (per invoice processed) · Tipalti (per payment)Accounts payable, invoicing, and compliance tools have the clearest outcomes in SaaS: invoices processed, payments executed, compliance checks completed. These are countable, auditable, and agreed on by both parties. Back-office AI that automates these tasks is structurally suited to outcome pricing — and buyers in these categories understand transaction-based billing from their payment providers.

Hybrid with Seat Floor

Examples: Notion · ClickUp · Monday.com · AsanaProject management tools are harder to reprice because outcomes are diffuse — “a completed project” depends on human judgment, scope creep, and priorities that change. Agents assist PMs rather than replace them entirely (for now). Hybrid pricing with a seat floor — enough licences for human orchestrators — plus consumption components for agent-generated tasks is the most defensible transition path through 2026–2027.

The Seat Compression Audit: Should You Act Now or Wait?

DIAGNOSTIC TOOL + REVENUE IMPACT MODELLERAccording to Bain’s analysis of 30+ SaaS vendors adding AI, what percentage simply bundled AI into existing per-seat pricing?

What pricing model did Intercom use for its Fin AI agent — and what growth rate did it achieve?

✅ Key Takeaways

- Pure per-seat pricing has fallen from 21% to 15% of SaaS companies in twelve months. Hybrid models have surged from 27% to 41% — the transition is structural, not cyclical. (Growth Unhinged, 2025)

- The February 2026 SaaSpocalypse wiped $285B from SaaS valuations in 48 hours — a reclassification event, not a panic. The market repriced per-seat SaaS as structurally overvalued in categories where AI agents replace human workers. (Taskade, March 2026)

- The Seat Paradox is real: the better your AI deployment performs, the steeper your seat reduction — and the steeper the drop in your vendor’s ARR. The model punishes success. Every SaaS founder in a human-replacement category must redesign their pricing before this hits their NRR.

- Intercom Fin proved outcome-based pricing at scale: $0.99 per resolved ticket, $1M to $100M ARR in 24 months. Salesforce Agentforce charges $2 per AI conversation. These are not pilots — they are production commercial models. (GTMnow via Bhavishya Pandit, 2026)

- 35% of SaaS vendors responded to AI by simply bundling it into existing per-seat pricing. Bain called this “structurally vulnerable.” Agents running 10x human volume under a flat fee will eventually make these products loss-making. (Bain & Company, 2025)

- The average enterprise wastes $21M per year on unused SaaS licences — a 14.2% increase from the prior year. 66% of provisioned licences are never opened. AI-driven headcount compression is accelerating this waste. (Zylo 2026 SaaS Management Index)

- Not all SaaS is equally exposed. Communication infrastructure, data storage, and security tools that agents use as infrastructure are defensible — even expanding. The risk is concentrated in tools that agents replace humans in using: support, SDR, back-office, compliance. Know which quadrant you are in.